MIC Global Raises US$6 Million Funding Round led by Launchpad Capital

01.25.2024

Company NewsPress Release

NEW YORK, NY, UNITED STATES (Jan. 25, 2024) – MIC Global (MIC), a full stack embedded microinsurance provider, today announced it has raised a US$6 million seed funding round. The round was led by Launchpad Capital, and joined by Greenlight Re Innovations, Ironsides Partners, and existing investors.

MIC Global provides simple and relevant microinsurance products for underserved consumers and businesses, embedded at the point of sale. Focusing on global insurance protection gaps, MIC’s digital reinsurance solutions provide payments to help people cope in the wake of unexpected loss of income, everyday risks, and identity theft. MIC currently operates in over 17 countries with plans to rapidly expand their geographical reach in 2024 through existing and new platform, insurer, and operating partnerships. With MIC’s in-house underwriting through Lloyd’s Syndicate 5183* and MIC Re, end-customers and business partners can expect long-term sustainable premiums, backed by Lloyd’s AA- ratings from Fitch Ratings, Kroll Bond Rating Agency, and Standard & Poor’s.

The funding will fuel MIC Global’s growth plans, including investments in infrastructure, talent, and market expansion.

Jamie Crystal, Co-Founder and CEO of MIC Global, said:

“We are pleased to welcome Launchpad Capital, GreenlightRe Innovations, and Ironsides Partners as strategic investors and partners to help fuel MIC Global’s continued growth as the preeminent embedded micro insurance provider. MIC is reimagining how insurance is bought and sold, and the additional capital will support the company’s global growth strategy with a focus on expanding our technology-enabled insurance platform to provide protection to people in both developed and emerging countries through our banking, mobile phone, digital/technology, insurance, and insurtech partners.”

“Jamie Crystal and Harry Croydon bring decades of global insurance and technology leadership to the embedded microinsurance opportunity. They built a team, technology infrastructure, and underwriting capacity that allows embedded distribution partners to rethink microinsurance. Innovators shouldn’t be restricted to ‘on the shelf’ products. MIC Global is the insurance sector’s equivalent to fintech’s sponsor banks.

“Over the past year our team and portfolio companies, Harmonic Financial Technology and Grid, have been impressed by the way the MIC team has enabled global insurance innovation with a ‘can-do’ attitude and ‘out of the box’ thinking. We all look forward to the future of this partnership.”

“We got to know MIC well by working closely with Jamie and Harry on an innovative glass insurance program, soon followed by an Income Protection program. They think differently about using technology to design and deliver high frequency, low dollar insurance programs that help customers address real-world risks.”

About MIC Global:

MIC Global is a full stack embedded micro insurance provider combining insurance capacity, embedded distribution, and scalable tech. MIC delivers simple digital reinsurance solutions to diverse insurance and platform partners, enabling individuals and small businesses to access relevant loss of income safety nets for when life happens. MIC’s innovative microinsurance products are tailored and embedded into platform ecosystems, adding value by enhancing the partner’s brand, differentiating their product, driving revenue, and attracting and retaining customers.

* Update Jan. 1, 2025: MIC Global Syndicate 5183 has closed as of the end of its 2024 Year of Account. MIC continues to offer Lloyd’s backed insurance underwriting as a Coverholder of Greenlight Re’s Syndicate 3456. Read more.

MIC Global: Simple Micro Insurance for Everyday Risks – Jamie Crystal, CEO [InsTech Podcast]

01.08.2024

Podcast

Ever wondered what MIC do? Why we do it? And how we are simplifying the insurance process? We have the podcast for you!

This insightful half hour gives you all you need to know about MIC for 2024!

Our CEO and Co-Founder Jamie Crystal features on InsTech‘s first podcast of 2024, joining Matthew Grant as they examine embedded micro insurance, dive into MIC as a company, and discuss our vision for insuring individuals with simple digital reinsurance products that protect their everyday risks. (28m 47s).

Key talking points include:

Understanding the concept of microinsurance

The problem MIC is solving – access to affordable products

Let’s talk about how we can collaborate on a digital reinsurance solution to help close protection gaps for your customers. Simply send us a few details below to get the conversation started.

New Year, New Password: Keeping Your Data Safe in 2024

12.27.2023

Cyber SecurityMiIdentity

With many of your trusted partners playing loose with your data and digital identity, is it time for you to make more effort? Six billion digital records were compromised in 2023 – more than those of 2021 and 2022 combined. (IT Governance)

So, it’s getting worse. The end of the year is time to do something. Many of us are now reflecting on the past year and thinking about how we can improve our habits. This coming year, we propose a different kind of resolution: maintaining your digital identities.

In today’s blog, we discuss what can happen with your compromised data, offer tips for improving your digital identity habits, and explore our solution to keeping your data secure: MiIdentity.

Let’s start with a few facts and figures from the last year…

Millions. Billions. Trillions.

An estimated 365 million people have been affected by data breaches in 2023 – slightly more than the entire population of the United States! (The Independent)

The largest data breach of 2023 happened to a UK-based digital risk protection company, DarkBeam, exposing a massive 3.8 billion records. (IT Governance)

In 2015, the global financial impact of cybercrime was estimated to be $3 trillion. It is now predicted that the annual cost by 2025 will be $10.5 trillion. That’s 5x the size of the UK’s GDP. (Forbes)

Consumers are feeling the effects. In a 2023 survey, 95% of studied organisations had experienced multiple breaches, and more than half of those breached were more likely to pass costs onto consumers. (IBM)

With these huge numbers in mind, is now the time you should be thinking about that 2024 New Year’s Resolution to finally take back some control and track your identity?

Why you should manage your data.

We all provide sensitive data to companies around the world, sometimes as simple as an email address to sign up to a newsletter, other times as complex as our health profiles when applying for insurance. We trust that it will be kept safely and used appropriately. You may not think too much about it when clicking submit, but outside of your control, your information (and by extension, you as an individual) instantly becomes vulnerable.

When a data breach occurs, your information can appear in shadowy corners of the internet – known as the dark web – and fall into the wrong hands. Primarily, cybercriminals use your compromised data for financial gain. With your stolen personal data (name, address, social security number, and date of birth, etc), cybercriminals can make fraudulent loan and credit applications, unauthorized transactions, and empty your bank accounts. With less information available, for example just an email address, you can be included in phishing email lists with the hopes that you may click and reveal more information about yourself.

Depending on how you are targeted, you can be left out of pocket and scrambling to secure your identity. But it doesn’t have to be that way.

Keeping your data secure.

As cyberattacks become more frequent with each passing year, we resolve in 2024 to protect our digital identities. Let’s look at four simple ways to do this.

1. Enable two-factor authentication (2FA) on all your accounts.

Where possible, enable this feature. 2FA adds an additional layer of security to your accounts, prompting users for a one-time password (via email/ SMS/ authenticator app), or biometric identifier (fingerprint/ facial recognition) be provided before allowing access to your account. If a hacker tries to remotely access your account, they will be unable to proceed. Check your account or app settings.

2. Be vigilant to phishing scams – spam emails, unsolicited texts, and unknown callers.

Phishing scams are becoming ever more sophisticated, in many cases looking identical to communications from real companies. You may receive an email asking to click to login and confirm account details (leading to a site harvesting user data), a text requesting confirmation of information (often linked to a premium rate number), or a phone call asking for all sorts of personal information (you know the ones!).

If you receive anything that seems suspicious: think twice, and do not click – unless it’s the delete button! If in doubt, contact the company in question directly.

3. Check for compromised data.

You can find out right now whether your email accounts have been compromised and leaked. Sites like Have I Been Pwned and Cybernews offer free tools that reveal in which breaches, if any, your email addresses and phone numbers have been leaked.

4. Change your passwords regularly and make them complex.

Having checked above, if your data has been leaked, there’s no better time than now to get your passwords updated. Regularly updating your passwords also means that if your details do get leaked, the data will soon be out of date, reducing the chance for malicious access – a good rule of thumb is every 90 days.

Your passwords should have at least 12 characters and include uppercase and lowercase letters, numbers, and special symbols – random jumbles make for even stronger passwords! There are many tools online that can do this and your device may even offer to set one for you, such as LastPass Password Generator or iCloud Keychain – make sure to keep your passwords in a safe, encrypted place.

Use MiIdentity, from MIC Global.

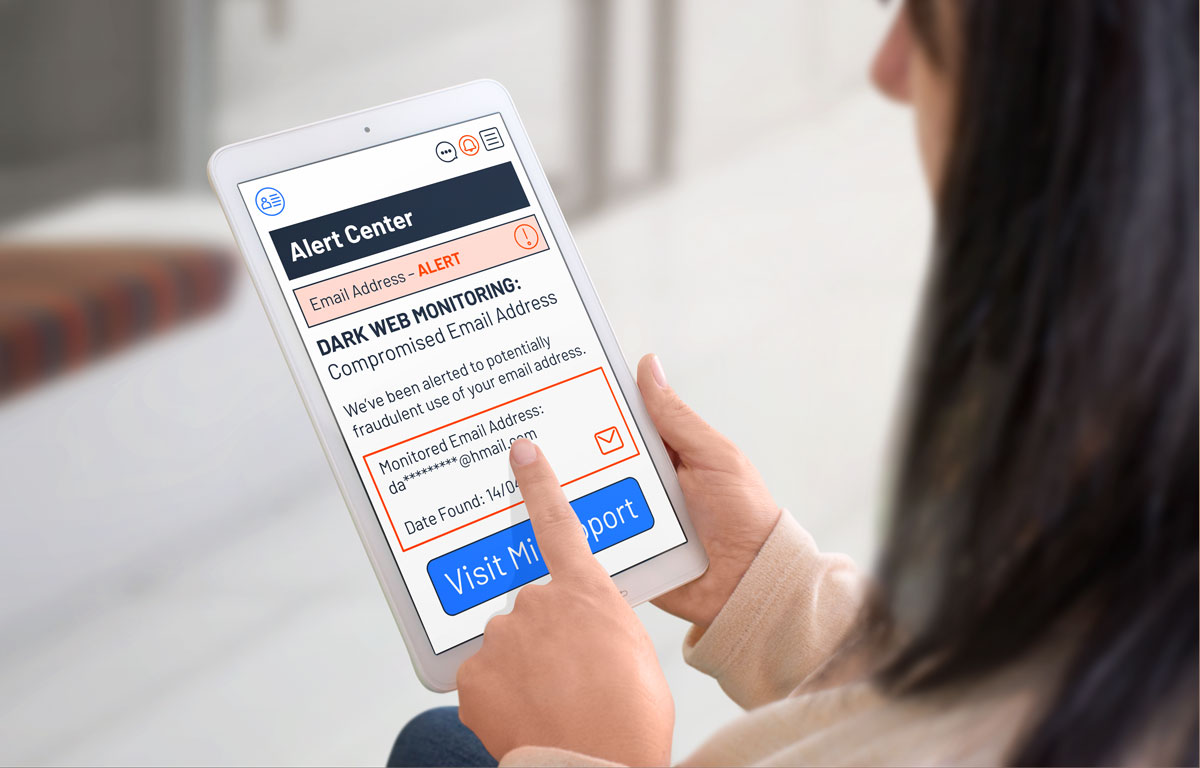

MiIdentity is our all-in-one identity monitoring and insurance platform, brought to customers via our insurance and platform partners. Upon registering, you provide the data that you wish to monitor, and our system proactively searches the dark web for listings and credit bureaus for financial activity. If your data is discovered or a suspicious transaction takes place, you are alerted with detailed information of your breached information – empowering you to secure your identity before it is used maliciously or further financial damage occurs.

In the event of theft and subsequent fraudulent use of personal identity documents, or monetary loss as the result of stolen or breached data, our Digital Identity reinsurance solution enables our partners to provide you with inconvenience payments to help deal with securing your compromised identity – such as replacing documentation or mitigating loss from a fraudulent transaction.

You are not alone in the identity recovery process. The MiIdentity platform is equipped with informative articles to kick-start recovery, and if further support is needed our team is available to help you through chat support and call operators.

Businesses can also benefit from MiIdentity. When a breach occurs, the platform becomes a critical tool in a full-scale data breach response. MiIdentity provides reports which can be used to measure the breach in real time, giving crucial data on the immediate and on-going impact as the breach progresses. Data from MiIdentity enables your recovery team to focus their efforts, and aids in creating specific messaging to support your customers.

Wishing you a secure 2024.

You wouldn’t leave your home or car unlocked for strangers to enter. So, as our lives and activities move increasingly online, we need to treat our personal data with the same respect and importance. With a few simple steps you can keep your data and digital identities safe on the internet and avoid being part of 2024’s statistics – a New Year’s resolution you can be sure to stick to next year and beyond!

“Happy New Year” from all at MIC Global.

Tell me more about MiIdentity

To learn more about our MiIdentity platform and digital reinsurance solution, visit our product page and get in touch with us below or via our contact form to discuss how we can help enhance your business’ customer cybersecurity offering and data breach recovery strategy.

Loss of Income Protection for Micro Entrepreneurs: From Risk to Resilience with Micro Insurance

12.21.2023

Gig EconomyMiIncome

Loss of income is an ever-present concern for micro entrepreneurs. The cause could be as simple as a broken phone or stolen laptop preventing fulfilment of over-the-phone or e-orders (plus the cost of repair or replacement!), sudden illness preventing work for a few days, or an overnight break-in closing a shop for repairs. Inconveniences that make them unable to sell their wares and services, causing immediate loss of income and monetary outlay.

MiIncome digital reinsurance is our loss of income micro insurance solution. We work with insurance and platform partners to support their own income protection products with tailored, trigger-based, reinsurance solutions that are relevant to their target demographic. MiIncome increases brand stickiness by showing platform customers that the brands that they already know and interact with have their backs when they’re faced with life’s inconveniences, boosting customer satisfaction and trust.

Wait, isn’t there already business interruption insurance?

While business interruption insurance sounds like the obvious solution, it generally isn’t suitable for micro entrepreneurs.

Business owners can protect their assets, employee wages, and incomes with business interruption insurance. Typically, these policies cover losses following large-scale disaster events that cause material property damage (building and stock) or create obstacles to business operations at a specified location. Events may include natural disasters, fire, flooding, and utilities failure (water, gas, and electricity).

This one-size-fits-all approach creates a protection gap for micro entrepreneurs. Often, these individuals don’t work from a fixed location or out of a commercial property (such as market and street traders or cottage industries). Many don’t hold stock or have employees to pay. However, they need protection for the financial inconveniences and income disruptions that result from large-scale events, and everyday life incidents that stall their business activities and ability to earn.

Let’s consider a food truck owner. Their business is mobile, they hold small quantities of fresh ingredients replenished daily, and work alone. They insure their truck for damage and theft, but as for their income, business interruption insurance simply isn’t a good fit for this micro business. If a flood were to hit and halt business, the owner is subjected to loss of income while unable to trade.

We are disrupting business interruption insurance.

Providing micro entrepreneurs with a relevant solution.

Our MiIncome digital reinsurance solution fills the gap left by traditional insurance. Unlike business interruption insurance, MiIncome is not dependant on large-scale events and consequential material damage to the business. Instead, through our platform partners, we cover the individual rather than their business.

Designed to protect individual’s income from life’s inconveniences, MiIncome helps our insurance and platform partners to provide quick payments to help cover their customers’ expenses when something happens that disrupts their ability to trade and earn. MiIncome is parametric, with defined pay-out triggers to ensure that a platform’s customers know exactly what they’re covered for, how much to expect, and for how long.

Working with you to support micro entrepreneurs.

Convenience, accessibility, and affordability are key to MiIncome. We collaborate with you to create a highly desirable MiIncome product tailored to the needs of your customers. This is embedded within your platform as an add-on to your core offering – differentiating your brand and creating a new revenue stream.

For example, MiIncome could be offered to micro entrepreneurs as part of a bank’s small business current account, ready to be called upon when income temporarily stops – perfect for the food truck owner mentioned earlier. In the digital world, it could be offered to sellers on an online storefront, for times that they are unable to fulfil orders due to personal circumstances – keeping sellers on the platform with an enticing benefit.

Your solution is integrated with our tech services via API, ready for when a customer needs to claim. Our claims process is powered by advanced AI technologies, allowing for rapid straight through processing. Claims can be received, assessed, settled*, and paid to our local insurance partners without human input, helping you to put money in your customers’ pockets fast – meaning that micro entrepreneurs can recover from whatever inconvenience is impacting their income and get back to business.

Helping micro entrepreneurs stay afloat.

Running a business comes at great personal risk. When unable to trade and faced with unexpected costs through no fault of their own, micro entrepreneurs are vulnerable to loss of income, and often don’t have insurance to fall back on. An affordable MiIncome safety net helps reduce that risk by ensuring they have a buffer in times of hardship, ready to pay out in just a few clicks.

So, for when life happens micro entrepreneurs, be sure to have a MiIncome solution in place to help keep them in business!

Tell me more about MiIncome.

Thanks for reading our article. To learn more about MiIncome, visit our product page and get in touch with us below to discuss how we can help your business put money in your customers’ pockets in their time of need.

MIC Global collaborates with Experian to bolster its MiIdentity product in India

12.20.2023

Cyber SecurityMiIdentityPress Release

NEW YORK, NY, UNITED STATES (Dec. 20, 2023) – MIC Global has entered a service level collaboration with Experian to strengthen the dark web and credit bureau monitoring service within MIC’s MiIdentity platform. MiIdentity is set to launch in India, bringing robust digital identity monitoring to individuals in the country’s rapidly growing online population.

MiIdentity is MIC’s proactive digital identity monitoring and insurance platform. The MiIdentity platform offers real-time dark web and credit bureau tracking, sending registered users alerts when their compromised data or suspicious financial activity is discovered. MiIdentity’s Digital Identity insurance component (provided as digital reinsurance via insurance platform partners) offers cover when individuals suffer a financial loss due compromised identity or financial data and documentation. In collaboration with Experian, Indian users can expect industry leading data monitoring, helping them to keep their data secure and maintained.

Experian is an international data analytics and consumer credit reporting company. The company’s core offerings include credit reporting, scoring models, and identity protection services, which empower businesses to assess creditworthiness and consumers to manage their financial well-being. Experian’s identity tracking expertise drives value and sets new standards in safeguarding digital identities, ensuring a secure and resilient online environment.

About MIC Global:

MIC Global is a full stack digital microinsurance company that provides embedded microinsurance for today’s digital world. MIC Global combines insurance capacity, in-country insurance licenses, world class distribution, and scalable tech. MIC Global creates embedded microinsurance solutions for platform companies that adds value by enhancing their brand, differentiating their product, driving up revenue, and attracting and retaining customers.

Experian is a global information services company that specializes in providing data and analytics solutions to assist businesses and individuals in making informed financial decisions. With a presence in 37 countries, Experian plays a crucial role in the financial ecosystem by collecting and analyzing vast amounts of data related to credit history, identity verification, fraud detection, and more.

Bouncing Back from Natural Disaster: Solving Individual and Economic Resilience with Micro Insurance

11.16.2023

Gig EconomyMiIncomeNatural Hazards

Flood. Storm. Earthquake. Wildfire.

These are among the most common forms of natural hazard events experienced around the world, and they’re becoming more frequent as climate change takes hold. These natural hazards can strike at any moment and often displace people, halt livelihoods, and can even affect country economies.

Resilience – “the capacity to withstand or to recover quickly from difficulties” – is key to individuals and economies coping with the aftermath of catastrophic events. In financial recovery terms, this means having an emergency fund available to aid recovery, but for many this simply is not possible. The insurance industry can offer a lifeline to enable individuals to weather the storm during a natural hazard event and after the dust settles, water retreats, or fires are put out.

In today’s blog, we consider the immediate financial effects of natural hazard events and how micro insurance products, such as MiIncome, can play a vital role in helping individuals and communities bounce back when disaster strikes.

Let’s consider someone many of us see in the streets every day or have seen on news stories…

Weathering the Storm

Ali is a bicycle rickshaw rider living in a country prone to extreme weather. As a gig worker, his income is based on his ability to work. For Ali, that’s riding and receiving fares, so any disruption can be costly. The last few years have been tough. The pandemic halted his earnings as people were mandated to stay in their homes, so he had no choice but to break into his savings to keep on his feet. Now, any emergency expense or loss of income is a major issue, as living week to week, he has little left to save.

Recently, the country has experienced an extended dry spell followed by torrential rainstorms that lasted a couple of days, with more rain expected. In Ali’s hometown, flash flood waters have risen rapidly, resulting in streets resembling rivers, and ground floors of homes and buildings like dirty swimming pools. Lives are on hold as flooding impedes movement, forcing many shops to close and utilities to be switched off.

Ali is attempting to work as usual, but with flood water up to his waist and being unable to see debris around his feet, he soon concedes and returns home, resulting in immediate loss of income. With more rain forecast, he has no idea when he’ll return to the road. To add insult to financial injury, with water and electricity supplies shut off, he needs to buy bottled water and much of his food could go to waste, requiring replacement when normality resumes – another inconvenience he could really do without.

A Global Protection Gap

Ali has an immediate need to access money to survive the flood, but dwindled savings will make day-to-day life challenging.

This begs the question – how can micro insurance be used to improve individual and national economic resilience in areas vulnerable to natural hazards?

MiIncome for Individual Financial Resilience

MiIncome digital reinsurance solution is our affordable, accessible, and relevant loss of income product which ensures people are adequately protected from threats to their livelihoods and incomes. We work with insurers and platform companies to support their own income protection products by tailoring MiIncome to their business and target demographic’s needs.

The MiIncome Resilience trigger provides coverage for loss of income due to natural hazards and extreme weather events. Coverage is parametric, enabling our insurance and platform partners to provide fast inconvenience pay-outs to their customers when insured events are met, to help navigate the issues they face in the moment. Going back to our earlier scenario, with coverage supported by MiIncome in place, Ali’s income gap will be softened, enabling him to afford emergency expenses, plug his lost income, and ride out the weather event.

Branching out further, MiIncome can be utilised at a national scale to help aid a country’s economy in the wake of natural hazards and extreme weather.

Where countries have a large proportion of gig and MSME entrepreneurs operating, a natural hazard event can temporarily remove many of these workers from the economy. Government-backed micro insurance programs can be offered to ensure that their local economy continues to operate and grow while people and small businesses recover from disaster.

Disaster Response Micro Insurance Case Studies

To better understand the practical impact of micro insurance on a national scale in post-disaster scenarios, let’s look at a few examples:

The Philippines: The Philippines is a nation that frequently faces extreme weather, including typhoons and earthquakes. Micro insurance programs, supported by both the government and local organisations, have allowed vulnerable communities to rebuild their homes and livelihoods after devastating events.

India: The Indian government has implemented micro insurance programs that specifically target agricultural communities. These policies provide coverage against crop failure due to extreme weather events, ensuring that farmers can recover and continue their agricultural activities even after a poor harvest.

Haiti: After the devastating earthquake in 2010, micro insurance played a crucial role in helping Haitian families rebuild their homes. Local organizations provided affordable micro insurance options, enabling communities to recover from this catastrophic event.

Helping People Recover from Natural Hazards with MiIncome Resilience

Natural hazards and extreme weather can hugely affect individuals in the moment, with a need for quick access to funds to cover short term loss of income, or in more serious circumstances provide cash to survive. Country’s economies can also suffer disruption while workers are unable to work and pay for goods and services.

With MiIncome Resilience, workers can access policies designed to help them in their hour of need with fast inconvenience payments*, which may provide a real lifeline when navigating a natural disaster. On a grander scale, governments can protect their citizens with government-backed insurance, but also gain a safety net that ensures that their economies remain stable and can weather the storm, while they focus on disaster recovery.

Tell me more about MiIncome Resilience

Thanks for reading our article. To learn more about MiIncome, visit our product page and get in touch with us below to discuss how we can help your business put money in your customers’ pockets in their time of need.

Data Breach Detected! How MiIdentity Empowers Corporate Recovery in the Aftermath of a Hack

11.07.2023

Cyber SecurityMiIdentity

In today’s digital age, where personal information is increasingly stored and shared online, corporate data breaches have become a prevalent threat. According to tech.co, at the time of publishing, there have already been at least 50 significant corporate data breaches and information leaks reported in 2023.

These breaches can have severe consequences, not only for the affected companies but also for their customers. Companies can hold sensitive personal and financial information on their customers, with breaches increasing the probability of financial loss and identity theft for individuals… and leading to a damaged reputation for the companies affected.

In this blog post, we will be focusing on the consequences of a data breach for businesses and customers, and how our MiIdentity platform and digital reinsurance solution serves as a vital part of a data breach recovery strategy, enabling companies to support their customers and mitigate the fallout after a breach.

A data breach from any company has the potential to affect your customers – in the last year, firms with massive customer and employee bases have fallen victim to breaches.

Social media platforms Meta, Twitter, Discord, and Reddit have been separately targeted with users’ personal information, login details and email addresses exposed; while a recent significant hack of Ipswitch’s MOVEit software stole sensitive employee personal data – such home addresses, bank details and National Insurance numbers – from hundreds of companies and government agencies worldwide including recognisable organizations such as Zellis, British Airways, BBC, Siemens, and New York City Department of Education, with the list growing daily as more companies come forward.

Organizations aren’t just vulnerable from malicious external attack either – breaches can also happen from within. A bug in OpenAI’s ChatGPT coding caused the AI chatbot to expose active users’ personal data to other users, highlighting the importance of internal security vigilance when using new technologies.

When any company suffers a data breach, it can seriously impact your customers. When their personal information falls into the wrong hands, they become vulnerable to digital identity theft – one of the most distressing consequences of the data breach. Your customers’ data will be permanently stored and displayed on the web, affecting them in the short and long term. Hackers often gain access to sensitive customer information, such as names and addresses, email IDs, credit card details, social security numbers, and banking credentials – depending on your industry your company could hold more data than this. Hackers and other criminals armed with this information can carry out fraudulent activities with your customers’ data for their own financial gains, for example to open new lines of credit and make unauthorized transactions and purchases… or they can simply cause mayhem with the data.

Digital identity theft leaves individuals vulnerable and grappling with the aftermath of repairing their credit history and attempting to reclaim their stolen identity which can often be impossible. The emotional burden of such violations can lead to prolonged stress and anxiety, as affected individuals deal with fraudulent charges, the laborious process of recovering lost funds, and proving their innocence in the matter. In the most severe cases, victims may suffer social impact and permanent financial damage, with long-lasting consequences for their overall financial well-being.

Your data breach response is critical.

While your company likely has many security features and safeguards in place intended to minimize the likelihood of a successful hack, the possibility is rarely reduced to zero. If your company does fall victim to a data breach, it becomes less about what security you have in place and all about how you respond – especially toward your affected customers. It’s a sink or swim moment for your company.

Once a breach is detected, your company must begin enacting its recovery plans and strategies to secure its systems that were affected, collect and retain any evidence around the breach, and protect its customers and their data. The first two points are tackled internally and are of the utmost importance to avoid further breaches, whereas the third point is public and a much more delicate operation – one wrong move can further damage your company’s reputation.

Next, it is vital to measure the impact of the breach…

How do you measure the impact to your customers and their data from the breach?

Introducing MiIdentity.

In response to the ever-present threat of data breaches for businesses, we have developed MiIdentity – a robust software solution with embedded micro insurance, designed to be an integral part of your organization’s cybersecurity suite and play a pivotal role in your data breach recovery strategy. MiIdentity supports companies and their customers through a combination of data leakage monitoring, security education, and financial reimbursement. MiIdentity measures the overall impact of personal data leakage so companies can comprehend and measure the impact of the breach.

It is important to note that MiIdentity does not prevent data from being hacked or breached data from being used. However, it acts as a powerful tool for an identity recovery strategy and customer reimbursement compensation processes after a breach occurs.

How does MiIdentity help your customers after a data breach?

Your customers interact with and provide personal data to an ever-increasing number of companies every day – many of which are high-profile targets like those discussed earlier – making it more than likely that eventually their data will be compromised. MiIdentity helps your customers after a data breach by notifying them when their data has been identified on the web or has been used to commit a crime. MiIdentity can tell a user where and how their data has been exposed and used – for example, if their data has been published on the Dark Web or used to acquire a loan.

MiIdentity comes with a web application where users can register their data for monitoring, such as phone numbers, email addresses, personal identifications, and financial and banking information. Our team supports all MiIdentity users through the recovery journey with helpful articles, chat support, and call operators. This can range from helping them with the process to rectify financial information and losses, to general security information like creating a strong password.

Where an individual suffers financial loss as a result of a breach, MiIdentity Digital Identity reinsurance supports our insurance and platform partners to provide inconvenience payments to mitigate the cost of securing the identity in question, such as filling in for lost monies after a fraudulent loan application. These timely inconvenience payments take the stress and financial burden out of securing compromised identities, as cash is available fast to get on top of identity recovery.

How does MiIdentity help your company after a data breach?

As your customers enrol in your MiIdentity offering and register identities for monitoring, we begin to collate monitoring data and provide comprehensive reports. Your company can understand the current condition of your customer data and then perform a thorough post breach analysis to measure the impact.

When your business is hacked, MiIdentity proves itself as a crucial tool as part of a full-scale response. Reports received after a data breach can be used to measure the fallout in real time, enabling your company’s response team to track the severity of the breach and arm them with crucial data to help recovery. MIC’s reports provide data on the immediate impact once a breach has been detected, and successive reports give your team clear insights into how a breach is progressing – tracking its growth and measuring the impact of the breach. With this data in hand, your team can focus their efforts internally and aid in creating specific messaging to support customers.

Although your customers wouldn’t wish to have their identity jeopardized; being diligent and having practical tools such as MiIdentity in place during the aftermath of a breach enables your company to support its customers with timely updates backed by measurable data. By playing an active role in helping them to recover from compromised identity, your company can potentially minimise reputation damage and customer trust.

When should your company start using MiIdentity?

MiIdentity can be implemented at any time – with maximum benefit received before a breach has occurred, giving you an understanding of your customers’ data at present. Once active, your customers can be encouraged to enrol in the platform and register their identities for monitoring. Reports start right away, giving your team a baseline of activity that can be compared against in the event of a data breach to accurately measure the fallout of stolen data.

The MiIdentity platform adds immediate value to your company’s offering, with alerts not only reserved for local data breaches but any instance of suspicious activity detected on a registered identity. When customer data is discovered after a data breach, your company can support them with alerts, education, and identity and monetary recovery – making your company a go-to destination for identity monitoring and keeps enrolled customers returning.

Leverage MiIdentity for your data breach recovery and supporting your customers.

A data breach to your company is a severe threat that can have a profound impact on your company and customers. It is imperative for your organization to prioritize robust cybersecurity measures, proactive risk management, and incident response policies to minimize the risk of a breach and actively address and limit the fallout if one occurs.

As more and more companies fall victim to data breaches, MiIdentity has been developed as a comprehensive solution to support corporate recovery efforts. When used alongside cybersecurity systems, MiIdentity gives your business an additional layer of reporting that aids a smooth recovery and demonstrates your commitment to your customers’ digital wellbeing.

This support goes beyond mitigating immediate effects of a stolen identity – it showcases your company’s dedication to customer satisfaction and strengthens the important bond of trust you’ve built with them.

Tell me more about MiIdentity.

To learn more about MiIdentity, visit our product page and get in touch with us below or via our contact form to discuss how we can help enhance your business’ customer cybersecurity offering and data breach recovery strategy.

Involuntary Unemployment: Protecting Employees from Income Loss

11.01.2023

MiIncome

“We’re sorry to inform you that your job role has been made redundant.”

“Budget cuts have forced us to make the difficult decision to terminate your position.”

“Thank you for all you’ve done but your services are no longer needed.”

It doesn’t matter how it’s worded, or how politely, becoming involuntarily unemployed is a tough, stressful situation for any employee to find themselves in. One of the biggest concerns is what they will do for income while out of work.

Typically, income protection insurance coverages are available to full- and part-time employees for when they are unable to work due to health (sickness or injury), through forced unemployment, or a combination of each. These coverages pay a percentage of a person’s salary – often until retirement for health related reasons – however in cases of unemployment, payments last for a set period, usually 12 months. Premiums are based on the percentage of salary that an individual wishes to receive and individual’s chosen deferred period (ranging from 30 days to 52 weeks). When unable to work for covered reasons, a claim is made, and monthly payments are given after the deferred period.

This sounds good on paper – but while income protection insurance provides a year of cover for unemployment, it can be quite costly to purchase. This is an added expense that many cannot justify in the current economic climate. In the UK for example, according to investment management firm Charles Stanley (as reported by Wales Online in October 2022), just 7% of adults claimed to have income protection in place and 18% were planning to give up or had already given up insurance policies to keep up with the rising cost-of-living. A year later, the cost-of-living crisis is still very much with us.

Based on these reported figures – and assuming that the figures are similar today and elsewhere in the world – it’s less of an insurance protection gap and more of a chasm!

The solution? Affordable involuntary unemployment protection.

With layoffs happening more regularly, the insurance protection gap is in urgent need of filling. Micro insurance is one answer to this issue.

Our MiIncome digital reinsurance solution has been designed to look after people’s short-term personal finances, by putting money in their pockets to cover the inconvenience of redundancy. The Layoff trigger has been specifically written to provide lump sum payments for a set period when made involuntarily unemployed. We recently launched a program with Grid in the US for this purpose, providing up to USD$4,000 over two months to laid off customers.

MiIncome, and micro insurance generally, brings the major benefits of affordability and convenience. Traditional insurance aims to provide comprehensive solutions that cover full repair or reparation costs with multiple steps to enrol and therefore can be very expensive because the limits are very high. Micro insurance on the other hand is designed to offer quick payments and target short term issues with subsequently lower limits, simplicity in operation and lower costs; with a goal of a couple of dollars a month and can be signed up to in just a few short steps. So long as employees meet basic requirements, they can be covered. Employees therefore get immediate cover to bridge a gap rather than full long-term income replacement coverage, but for many this is an affordable safety net while they find a new job.

The next question is, how do employees access MiIncome and how does it work?

How does a MiIncome digital reinsurance solution work?

We work with insurers and platform partners to reach their customers through integrated solutions. Working closely with you: we tailor MiIncome to your needs, developing a product that is highly relevant and desirable to your target market.

Your MiIncome digital reinsurance solution is developed with our Operations and Underwriting teams, who analyse your proposition and set pricing, terms, and conditions.

To bring the product to life, our tech and operation teams work with you to integrate it with your app or web service via API. We hook into your forms to receive and validate submissions, ensuring that customers and employees are eligible for coverage.

When individuals need to claim, our AI powered process quickly assesses and settles*, providing timely payments to our local insurance partners, so that you can help your customers get on with their lives with less financial burden.

Furthermore, MiIncome doesn’t just provide benefits to your customers – it differentiates your product offering from your competitors, creates a new revenue stream, and adds value for your customers with boosted retention and satisfaction. Your customers can trust that you’ve got their back when faced with layoff.

Enabling your customers to bounce back from involuntary unemployment.

No-one wants to receive news of unemployment, and employers don’t want to have to give it either! With MiIncome protection in place, employees have peace of mind that should they receive notice, they have a financial safety net to continue paying their household and living expenses while finding a new job. Providing MiIncome shows that your company cares about the financial wellbeing of your customers.

So, for when professional life happens to your customers , be sure to have a MiIncome solution in place to help them get back to living it!

Tell me more about MiIncome.

Thanks for reading our article. To learn more about MiIncome, visit our product page and get in touch with us below to discuss how we can help your business put money in your customers’ pockets in their time of need.

A twisted ankle for a cycle courier. Laryngitis for a temporary customer call operator. Flu for a cabin crew member.

While these may not sound like a big deal, for the individuals affected it can lead to struggles paying the rent, putting food on the table, accessing medical care… being able to afford the crucial things in life. The gig workers in the examples above will be unable to work and will not receive a portion, or any, of their usual income for the duration of their recovery.

This is a huge problem for gig workers globally, who often do not receive employment benefits when unable to work and have difficulty getting income protection. What can people do to safeguard themselves against income loss in the gig economy which is not typically served by income insurance providers? How can this insurance protection gap be filled with micro insurance products such as MiIncome digital reinsurance?

Life happens…

First, let’s consider a few scenarios. These stories could happen to anyone, but can cause real problems for the gig workers.

A cycle courier is also a keen amateur soccer player. One weekend while training he trips and badly sprains his ankle. It’s enough to visit the Emergency Room, and he’s prescribed pain killers and a month of rest to recover – or else risk further damage. Being a gig worker, he needs to be able to complete jobs to earn an income. A month off his bicycle will put a real strain on his finances – he has rent and expenses to pay, and on top of that an outstanding medical bill and prescription pain killers to cover.

An office support temp working as a customer call operator has a fun night out planned. She and her friends visit a karaoke bar, where they serenade the crowd into the early hours. Next morning, she awakes to a burning throat and can barely speak… clearly, she won’t be answering calls today! An online diagnosis suggests laryngitis and that she should rest her voice for at least a week – no matter, she can request to move to a different support role. While this flexibility is convenient, the gap in her income while she is reassigned will not be. With less income for the month, she’ll need to prioritise her expenses and stretch what’s left.

A cabin crew member is home for the week. While visiting family, she picks up a case of flu. Now, airline policy means that she will be grounded until she has recovered. Of course, this means that she will not earn her flight hour bonuses and layover allowances, which she relies on to top up her basic salary. She knows that her basic salary isn’t enough to comfortably live on, so this month is going to be tough on her wallet. She loves her job, but the risk of being grounded and losing income through illness is an aggravation she could do without.

Gig workers are vulnerable to loss of income

Gig workers – employees, contractors, and freelancers in the gig economy, such as those described – rely on their ability to work to make a living. Gaps in income due to injury, illness, and personal reasons are not typically accounted for by their employer. So, while these sorts of jobs can be highly rewarding – providing scalability, flexibility, or even the chance to see the world – ‘when life happens’, workers are vulnerable to fluctuations in income when they are unable to work.

Nobody wants to hide away to avoid unexpected illness and injury, but at the same time everyone needs to safeguard their ability to earn a living.

The simple solution for protecting gig worker’s income income from life’s inconveniences

The gig economy comes with its own set of challenges when it comes to applying for personal income protection. Generally, insurers require a minimum number of hours to be worked per week, which those working zero-hour contracts and gig-to-gig are not always able to guarantee. So, it’s often the case that income protection insurance through traditional insurers is simply not accessible. It’s easy to see how an insurance protection gap has formed.

Which is where embedded micro insurance comes into play. This style of insurance isn’t concerned with how many hours a person works, who they work for, or when they work. Micro insurance is generally available to anyone who has a need to access quick payments in order to soften the financial blow an unexpected event. With defined parameters, customers know exactly what they’re covered for and what will trigger a pay-out. This is perfect for gig workers who may suddenly find themselves unable to work.

Loss of income micro insurance products – such as our own MiIncome digital reinsurance solution – are accessed via relevant platforms and services rather than insurance companies. This could be an add-on to a bank’s credit card scheme or as part of a virtual wallet app’s offering. Opt-in products are offered through a customer’s account for a micro premium, which can be leveraged as required – helping them maintain their income through adverse health and events. These embedded insurance products are convenient and affordable, making them a real financial lifeline for those without adequate income protection.

Platform companies can also benefit from implementing an embedded micro insurance solution. Typically, high employee turnover rates are experienced by the gig economy and industries that don’t guarantee sick pay – such as airlines, hospitality, and retail. To counter concerns about income fluctuation, platform companies can offer loss of income schemes as a perk to their employees, enabling them to provide coverage in times of need. This can boost employee retention and job satisfaction, as staff have easy access to income loss cover – making them less likely to get frustrated with income gaps and look for less risky employment elsewhere.

This is where your business comes in!

Your business can provide a safety net to your customers and employees with MiIncome

MiIncome is our popular loss of income suite, which looks after people’s personal finances when they’re unable to work – we help our insurance and platform partners put money in people’s pockets. This specialized embedded micro insurance product is designed to offer short-term income security for individuals engaged in full- and part-time jobs, self-employment via independent contracts, gig work, and moonlighting and freelancing while operating through a platform company.

MiIncome supports your own income protection program.

We work with you to tailor MiIncome’s triggers to your company’s specific needs, creating a product that is highly relevant and desirable to your market – whether that’s your customers or employees. MiIncome also has the added benefits of creating an additional revenue stream, differentiating your company and strengthening customer trust and satisfaction in your brand.

The Health trigger has been developed for situations just like those discussed here. In the event of sickness or injury that prevents an insured individual from working, lump sum payments are made to help them cover their essential expenses. This helps mitigate the income gap burden faced by many gig workers, who are now able to recover comfortably without financial woes.

We integrate our MiIncome solution with your company’s platform via API. When a claim is made, it is rapidly assessed and settled* by an AI powered automated process. So long as all the parameters for claim are met, quick payments can be made to our local insurance partners, meaning insured individuals can have money in their pockets fast. This speed of payment is a massive benefit to gig workers – many of which are used to being paid daily or weekly.

Making the best of a bad situation

Being ill or injured and unable to work is a difficult position to be in for anyone, especially for gig workers. With MiIncome in place, insured gig workers have peace of mind that income gaps due to adverse health are covered. As for gig economy employers offering a MiIncome scheme, you can be safe in the knowledge that when your workers are fit to return to work, it will still be with you.

So, for when life happens to your customers and employees, be sure to have a MiIncome solution in place to help them get back to living it!

Tell me more about MiIncome

Thanks for reading our article. To learn more about MiIncome, visit our product page and get in touch with us below to discuss how we can help your business put money in your customers’ and employees’ pockets in their time of need.

Safety Nets on the Go: Connected Cars, In-car Commerce and Micro Insurance

10.04.2023

Micro Insurance

As developments in technology and commerce accelerate at rapid speeds, we’ve gone from physically shopping in-store, to mail orders via telephone, to digital online orders at the touch of a button in a relatively short space of time. Now, retailers and services are targeting consumers on their commutes.

“In-car commerce” is the latest way to shop, with advances in on-board technology making this new commerce opportunity viable for the micro insurance industry to innovate within.

In this article, we take a look at how connected cars enable micro insurance and consider a few examples of how micro insurance incident protection can be used to provide a safety net and improve the driving experience.

Nearly 30 years on from OnStar’s inception, huge leaps forward in technology have brought mobile networks, multi-touch screen dashboards and other things that consumers are used to on a tablet device to the fingertips of drivers.

In-car technology as an enabler for micro insurance.

Speaking of Hollywood – once fantastical gadgets reserved for James Bond’s vehicles are now very much a reality. Cars are increasingly being produced with exterior and interior cameras as standard, to aid drivers on-the-road and improve vehicle security. AI is also finding its way into the car – notably through assistants such as Apple’s Siri and Amazon’s Alexa – to assist the driver and passengers in real-time. Just don’t expect them to help you escape from a heavily guarded parking garage!

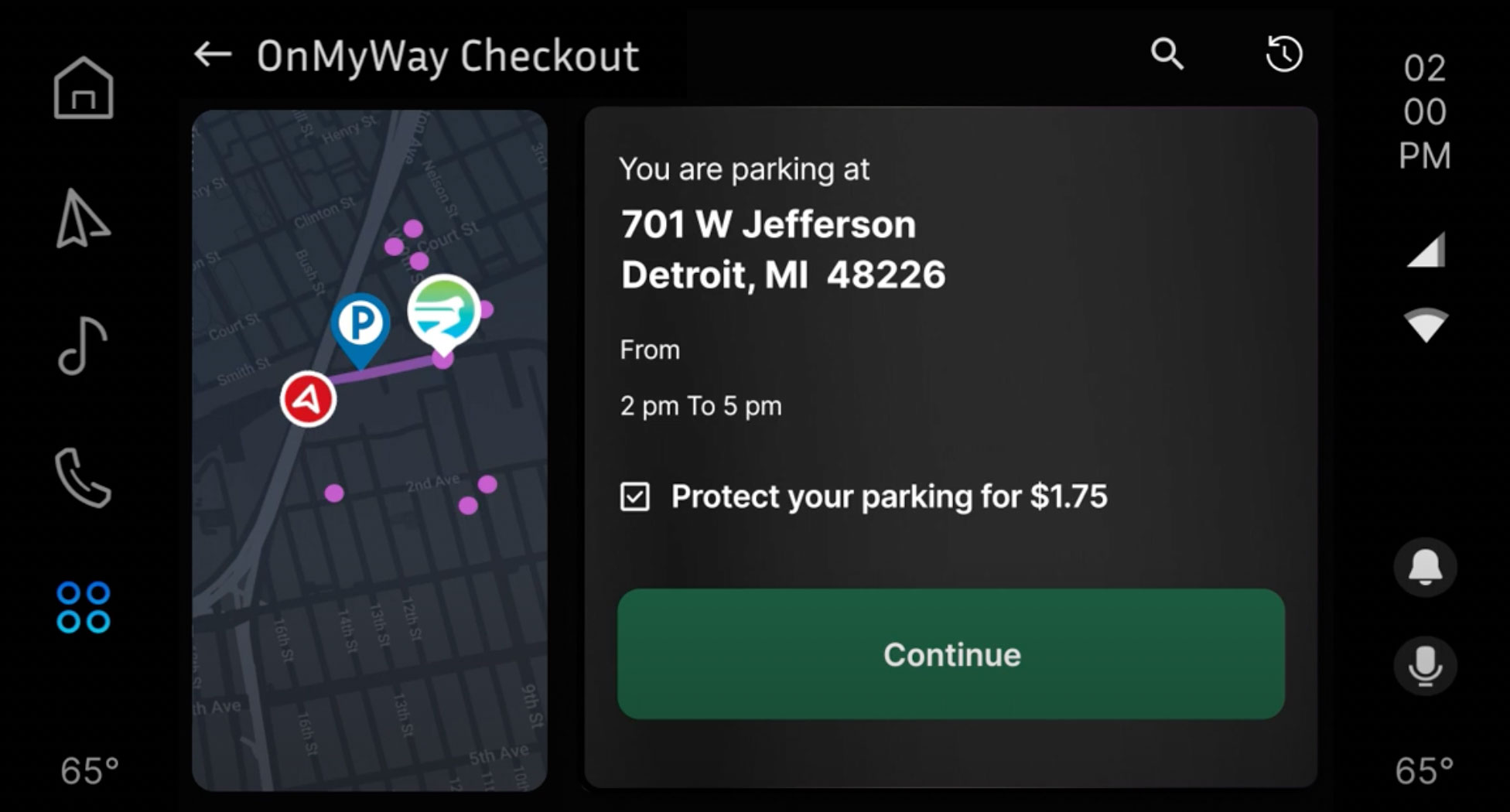

E-commerce is now in cars too – dubbed vehicle or in-car commerce in the automotive industry. Through a car’s dashboard system, consumers set up their payment information enabling them to make purchases for goods and services such as EV charging, fuel, and parking directly from their vehicle. This is of real benefit and an improvement in safety for drivers, who no longer need to use a smart phone at the wheel – or even leave their vehicle! – to make everyday purchases and links real-time location data to the services on offer.

Micro insurance is driven by data, analysis, and specified events. Connected cars are now collecting the types of data ideal for developing embedded micro insurance solutions, such as location, vehicle telemetry, image and video monitoring, and more! These data points can be used by claims handling AI to analyse and make informed decisions, providing drivers with real-time payments.

Representing a $230 billion commerce opportunity in the US alone, according to PYMNTS and P97 Networks, in-car commerce has the potential to become a major revenue channel for businesses – and this includes insurance.

What does this mean for retailers and micro insurance?

When purchases are made through a car’s dashboard, such as those mentioned earlier, embedded micro insurance can be used to enhance the value of the purchase – both for the retailer and customer. Micro insurance solutions provide an additional revenue stream for the retailer, while building customer trust and providing peace of mind that should the worst happen, enrolled customers are covered.

In the spirit of GM’s pioneering system, micro insurance can be applied to the automotive industry to offer convenient protections for vehicle security, driver safety, assistance with the cost of repairs, and protecting against on-the-road inconvenience. Let’s consider a few examples that could benefit from micro insurance.

Talk to us about MiIncome Mobility digital reinsurance and in-car commerce.

Smart Camera Parking Protection.

Anyone that drives a car has likely used a car park, purchasing a ticket for the duration of their stay. Drivers don’t know whether the car is completely safe, but it’s a risk that must be taken. Adding micro insurance to this transaction is one way to give drivers peace of mind over leaving their car – such as our recent partnership with Mavi.io’s OnMyWay Commerce platform. With the assistance of an integrated camera monitoring the vehicle – if a window is broken while the car is parked, the micro insurance product automatically provides an inconvenience payment for the driver to rectify the damages.

Since transactions are completed through the car’s dashboard navigation system, new and innovative applications for micro insurance can be considered. Innovation & Tech Today reports that booking restaurant reservations is a popular theoretical use case in consumer surveys. Micro insurance could be applied to this transaction, providing protection for if the driver becomes stuck in traffic – through the combination of on-board navigation, traffic monitoring, and time keeping, inconvenience payments can trigger to soften the disappointment of a missed reservation.

AI Monitored Vehicle Servicing and Repairs

Cars need to be serviced throughout their lifetimes to ensure optimum performance. This wear-and-tear servicing is not generally covered by car insurance, so falls to the driver to pay as required. Car manufacturers are creating AI damage detection tools to aid drivers and mechanics with repairs and servicing, boosting driver confidence in the vehicle and productivity for the repairers. Micro insurance can hook into this data collection process, providing payments when the AI detects a fault or service due, enabling drivers to immediately afford repairs rather than delaying.

Sharing Economy Car Insurance

Micro insurance is also perfectly suited to peer-to-peer car sharing – and according to Turo’s director, was originally created for that specific purpose. Drivers who share cars on an occasional basis have no need for a yearly insurance policy, so micro insurance fills this gap by providing timed trip insurance. This ad hoc insurance is typically purchased via an app, though with the advances in connected-car technology, these transactions could be completed through the vehicle’s dashboard.

This example of P2P car-share insurance could be taken one step further. Cars used by multiple drivers could require users to log in to their personal insurance profile on a dashboard app to purchase or verify their trip insurance before the car can be engaged. This would provide security to the car’s owner and reduce the likelihood of uninsured drivers on the road, making travel safer for everyone.

In time, as built-in telematics sensors become available, it is expected that unique risk profiles can be generated for individual drivers, saved to their user profiles. This will enable tailored micro insurance policies to be offered to the driver, rather than basing the policy on the vehicle.

The In-car Commerce Opportunity

With in-car commerce representing such a large opportunity for revenue, it’s only natural for the insurance industry to look for ways to integrate and support new customers. This opportunity is not just revenue driven – there is also the chance for new micro insurance innovation. Connected in-car technology is collecting valuable data which can be used to develop inventive solutions to problems that inconvenience drivers every day. As in-car technology becomes more advanced and abundant, new partnerships with like-minded tech companies are a practical approach to enhancing drivers’ vehicle-based transactions.

Micro insurance is parametric in nature – triggered by specific events – and is purchased at a point of sales where it is often embedded with a relevant adjacent product giving access to insurance when needed rather than as a blanket coverage. Coupled with its convenience and affordability, this makes in-car commerce a prime untapped target for the micro insurance industry.

Contact us to see how MIC Global can help your business benefit its customers and employees with an embedded micro insurance solution, or simply send us your email address above to get started.