Why MIC Global’s growth model compounds instead of plateaus

By Harry Croydon, Co-Founder, President & COO.MIC Global

Most insurance companies run on a pipeline. Leads come in, policies go out, renewals follow. Growth is a function of headcount, marketing spend, and distribution relationships — all of which cost money and plateau over time. The model works. But it does not compound.

The problem with the pipeline

Traditional insurance grows linearly. Add a salesperson, write more policies. Increase the marketing budget, generate more leads. The pipeline has no answer for the growth rates the best digital platforms post: fintechs doubling their user base in twelve months, gig economy operators crossing borders in a quarter.

MIC Global was built to serve those platforms. To do that seriously, our growth model had to match theirs. The pipeline was never an option.

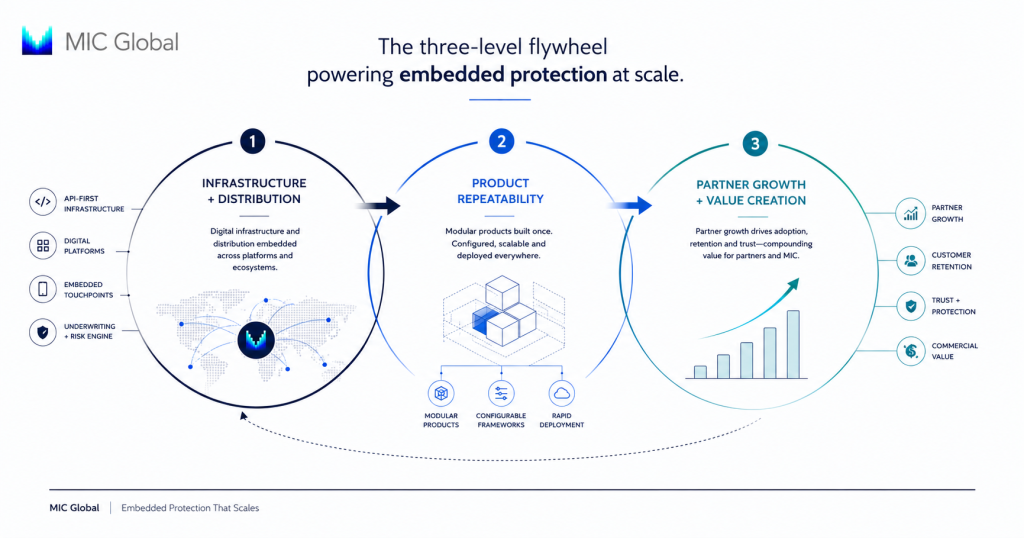

The flywheel idea: why three levels

A flywheel is a growth model built on momentum. Each action adds energy to a spinning wheel. The heavier and faster it turns, the less effort each subsequent push requires. Amazon mapped this principle in its earliest shareholder letters: more customers attract more sellers, more sellers attract more customers, lower costs from scale attract more of both. The wheel becomes self-reinforcing.

Most businesses that adopt a flywheel model operate at two levels. MIC Global operates at three. The third level is where the economics change.

Wheel one: capacity and partners

The first wheel connects our Lloyd’s Coverholder status and reinsurance relationships which is our underwriting backbone to a growing network of digital distribution partners: platforms, fintechs, lenders, and gig economy operators across the US and globally.

The logic is direct. The more partners we add, the more data we accumulate. More data means better underwriting, faster product development, and sharper pricing. Better products attract more partners. The wheel starts turning.

MiIncome™ is the engine here: embedded income protection designed to sit natively inside a partner’s platform. Not bolted on. Not a redirect. Protection felt as a product benefit, invisible as a policy. Partners including inDrive, QIC, Rhino, and ASNA are part of this wheel today, each adding momentum.

One thing that keeps the first wheel nimble: MIC Global carries no long-tail catastrophe exposure, no large-limit liability. The platform is built to move fast.

Wheel two: products and scale

The second wheel engages as the first accelerates. As our partner network grows and our data deepens, we develop and deploy new products at a pace and cost that traditional insurance infrastructure cannot match.

MiIncome™’s trigger architecture makes this possible. Involuntary job loss. Natural hazard income disruption. Gig worker accident cover. Trip cancellation. Weather inconvenience. Each trigger is modular, repeatable, and deployable across new markets in a fraction of the time a traditional product build requires.

Every product we add strengthens what we can offer a partner. Every market we enter expands the compliance and fronting network they benefit from. A partner launching in the US today can expand into India, Latin America, or Southeast Asia with MiIncome™ already positioned to support that move.

The second wheel also collects data at scale: claims data, behavioural data, loss ratios by trigger type and geography. That feeds back into underwriting, pricing, and product design. The flywheel tightens.

Wheel three: partner growth compounds our growth

This is the level that makes MIC Global’s model different from any two-level flywheel, and the reason we believe our growth potential is comparable to the platform businesses we serve.

The partners we work with are not passive distributors. They are flywheel businesses in their own right — platforms actively growing their user bases, deepening their ecosystems, and expanding into new markets. And this is where our model does something a conventional insurance relationship cannot: we help them do it.

We do not just grow when our partners grow. We help them grow. Embedded income protection — properly positioned — becomes a product feature that improves acquisition, deepens retention, and extends customer lifetime value. When a partner integrates MiIncome™, they are not bolting on an insurance policy. They are adding a commercial asset. Their acceleration adds to ours. Ours feeds back into theirs. The right partners do not slow the wheel. They spin it faster.

The first wheel is running. The second is accelerating. The third is what makes the whole model self-reinforcing — for us, and for the platforms we work with.

Why now

The income protection gap is not a niche problem. According to the International Labour Organization, more than 4 billion people globally have no meaningful social protection coverage. In the US alone, more than half of adults cannot cover three months of expenses from savings. The gap is structural. Existing solutions are priced and distributed for a different era. The opportunity to reach underserved people through digital platforms they already trust has never been more accessible.

Traditional insurers were not built to close this gap. Their distribution models, product timelines, and cost structures were designed for a different customer relationship — one that reaches far fewer people, at far higher price points.

MIC Global was built for this gap: with the flywheel architecture, the AI infrastructure, and the partner network to make embedded income protection a standard feature of digital life.

The first wheel is running. The second is accelerating. The third is what makes it self-reinforcing.

The right embedded protection partner should make your platform stickier, your customers more loyal, and your proposition harder to replicate. If that sounds like the right conversation, let’s have a chat.

About the Author

Harry Croydon is Co-Founder, President and COO of MIC Global. Connect with Harry on LinkedIn